High-income professionals often juggle complex finances, legislative changes, and competing goals. Treating wealth management like construction, a financial architect creates a resilient blueprint for lasting security.

Understanding the Financial Architect's Role

Just as an architect designs a building down to every beam and finishing, a financial architect crafts comprehensive, structured wealth strategies tailored for high earners. By integrating tax optimization, investment planning, lending structures, asset protection, and estate design, they ensure your financial foundation remains strong through market cycles and life changes.

This role goes beyond selecting products. It involves a holistic view—mapping out your current position, aligning resources with objectives, and providing ongoing oversight to adapt to new risks and opportunities.

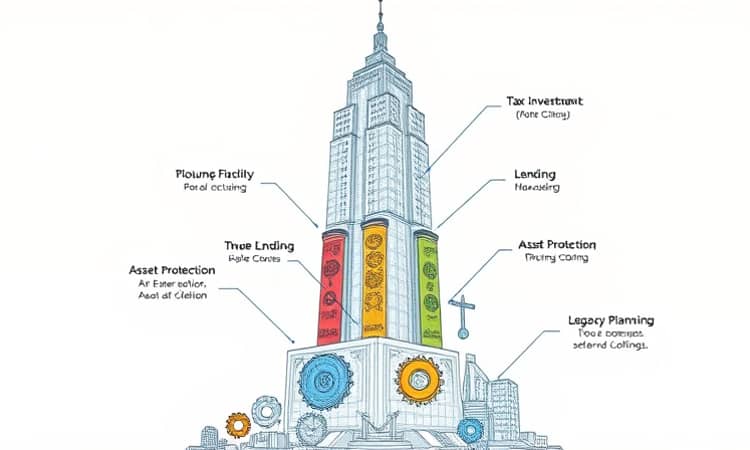

The Five Pillars of Wealth Architecture

A robust blueprint rests on five core pillars of wealth architecture. Each pillar functions like a structural support, working together to hold up your long-term plan.

- Superannuation and retirement optimization: Maximizing concessional contributions and catch-up allowances for sustainable growth.

- Tax-aware investing and lending structures: Using debt recycling, trusts, and investment bonds to reduce liabilities.

- Asset protection and insurance planning: Implementing legal entities and insurance wraps to safeguard wealth.

- Estate and legacy transfer strategies: Establishing trusts, succession plans, and philanthropic vehicles.

- Risk management and cash flow planning: Building emergency reserves and inflation-adjusted income streams.

By coordinating these pillars, clients achieve comprehensive financial design with long-term resilience that adapts as their lives evolve.

Understanding how these tactics interrelate helps prevent siloed decisions and costly oversights.

From Blueprint to Build: The Process Explained

Effective wealth architecture unfolds in three phases: discovery, blueprint design, and implementation. Each stage mirrors building a structure—from laying foundations to continuous maintenance.

- Background and discovery phase: Gathering data on income, assets, liabilities, goals, and risk tolerance.

- Blueprint and design phase: Modeling scenarios, analyzing trade-offs, and outlining action steps with timelines.

- Build and implementation phase: Executing recommendations with tax, legal, lending, and investment specialists while monitoring progress.

During discovery, advisers map out your current landscape. In the blueprint stage, they stress-test strategies to transform high income into long-term security without compromising flexibility.

The build phase brings together accountants, lawyers, lenders, and insurance experts to turn the plan into reality. Regular reviews ensure your blueprint evolves with legislative changes, market conditions, and personal milestones.

Overcoming Common Challenges

Many high earners assume that income alone guarantees wealth accumulation. In reality, unseen drains like inefficient borrowing, suboptimal super contributions, and uncovered risks can derail progress.

Legislative shifts—such as Division 293 and Division 296 changes to superannuation tax rates in Australia—add layers of complexity. Missing a contribution deadline or misclassifying an asset can trigger additional tax liabilities or penalties.

A financial architect applies rigorous inefficient tax strategies and legislative risks analysis to identify vulnerabilities early, closing gaps before they threaten your objectives.

Case Study: A Medical Specialist's Journey

Dr. Smith, 44, earns A$480,000 annually and holds A$2.7 million in superannuation alongside a A$3.5 million property portfolio. Despite a strong net worth, Dr. Smith lacked an interlinked strategy and faced escalating tax on excess contributions.

In the discovery phase, key goals emerged: fund two children’s private educations, build a charitable legacy, and retire by age 60 with a steady income. The blueprint proposed increased concessional contributions, strategic debt recycling on properties, and a discretionary trust for philanthropy.

During implementation, Dr. Smith’s team restructured mortgages to unlock equity for diversified investments, optimized super contributions to avoid additional tax, and secured professional indemnity and critical illness cover. Over 18 months, after-tax returns climbed 15%, annual tax outlay dropped by 8% of income, and philanthropic objectives were funded through a donor-advised fund.

Key Takeaways and Next Steps

- Define SMART goals aligned to your values and timeline to guide every decision.

- Coordinate tax, super, borrowing, and estate elements to avoid unintended consequences.

- Implement risk management—emergency funds, insurance, and legal shields—to protect capital.

- Schedule annual reviews to rebalance your blueprint against life events and market shifts.

Viewing your financial life through an architectural lens brings coherence to complexity. With a solid blueprint and expert team, you can build financial foundations that stand the test of time.

Frequently Asked Questions

What services does a financial architect provide? They offer end-to-end design, execution, and oversight of wealth strategies covering investments, lending, tax, asset protection, and estate planning.

How is this different from wealth management? Wealth management often focuses solely on portfolio performance. A financial architect creates a holistic blueprint, aligning every financial decision with your long-term vision.

Who benefits most from this approach? Professionals with complex finances—medical specialists, executives, business owners—who require a coordinated strategy to maximize after-tax wealth and ensure smooth intergenerational transfer.