Financial stability begins with a clear vision for your future. Transforming dreams into actionable plans requires setting goals across different time frames.

This approach empowers you to take control of your money and build the life you desire. Short-term goals under one year provide the immediate momentum needed to stay motivated.

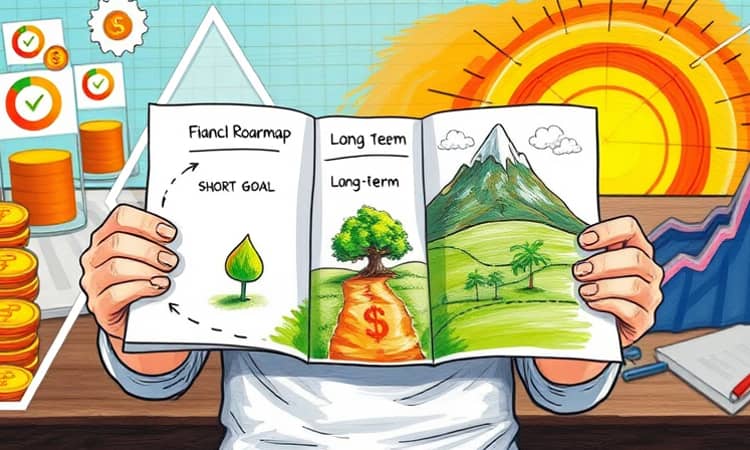

As you progress, medium and long-term goals ensure sustained growth and security. A structured roadmap for financial success can turn aspirations into reality with discipline and strategy.

Understanding the Time Frames

Goals are categorized based on their time horizon to make planning manageable. Short-term goals are those you aim to achieve in less than 12 months.

They offer quick wins that boost confidence and keep you on track. Provide quick wins and motivation through immediate accomplishments like paying off small debts.

Medium-term goals span from one to five years. These require more planning and discipline than short-term objectives.

Long-term goals extend beyond five years. They involve big-picture items that demand consistent effort over time.

- Short-term: Under 1 year, for immediate plans.

- Medium-term: 1-5 years, for mid-range objectives.

- Long-term: 5+ years, for lifelong aspirations.

Common Financial Goals by Category

Identifying typical goals helps you start your own list. Short-term goals often focus on immediate needs and small victories.

- Establish an emergency fund.

- Pay off credit card debt.

- Save for a vacation or wedding.

- Cover minor home repairs.

Medium-term goals bridge the gap between short and long-term plans. They often involve significant purchases or debt reduction.

- Saving for a down payment on a home.

- Paying off student loans or a car.

- Building credit history from scratch.

Long-term goals are about securing your future and achieving major life milestones. These require long-haul commitment and smart investing.

- Funding retirement accounts fully.

- Buying a house outright.

- Saving for a child's college education.

- Starting your own business venture.

The SMART Framework for Effective Goal Setting

The SMART criteria turn vague wishes into achievable targets. Each letter stands for a key principle in goal formulation.

Specific goals define exactly what you want to accomplish. Instead of "save money," aim for "save $5,000 for a car down payment."

Measurable goals use concrete numbers to track progress. Set monthly savings targets to see how close you are to your aim.

Achievable goals are realistic given your current financial situation. They should challenge you without being impossible.

Relevant goals align with your personal values and desires. This increases motivation and ensures the goal matters to you.

Time-bound goals have a clear deadline for completion. Breaking them into smaller timelines helps maintain focus.

- Specific: Define the exact outcome.

- Measurable: Use numbers and milestones.

- Achievable: Keep it realistic and attainable.

- Relevant: Ensure it aligns with your life.

- Time-bound: Set a firm deadline.

Prioritizing Your Financial Objectives

Not all goals can be pursued at once, so prioritization is crucial. Start by assessing your current financial position thoroughly.

List all your goals and rank them by importance and urgency. Emergency fund and retirement savings should typically come first for security.

This ensures you cover essentials before moving to discretionary items. A clear order prevents overwhelm and guides your budgeting efforts.

- Focus on basic needs like food and shelter.

- Build an emergency fund for unexpected expenses.

- Contribute to retirement accounts regularly.

- Pay down high-interest debt aggressively.

- Allocate remaining funds to other goals.

Practical Strategies for Implementation

Breaking down large goals into smaller steps makes them less daunting. For example, save a set amount each month toward a down payment.

Budgeting frameworks help allocate income effectively across needs and goals. The 50/30/20 rule is a popular method for balancing expenses.

Automation removes the manual effort from saving and investing. Set up automatic money transfers to designated accounts to stay consistent.

Tracking progress with tools like apps or spreadsheets keeps you accountable. Regular check-ins allow for adjustments if circumstances change.

- Use digital apps for real-time monitoring.

- Create separate savings accounts for specific goals.

- Celebrate small victories to maintain motivation.

- Write down goals and review them periodically.

Real-World Examples to Inspire Action

Seeing practical scenarios can motivate you to start your own journey. A couple saving for a wedding sets a two-year timeline with monthly contributions.

Another individual aims to travel by cutting back on dining out for eight months. Pay off credit card debt over two years with structured monthly payments.

These examples show how breaking goals into chunks makes them achievable. They highlight the importance of consistency and minor lifestyle adjustments.

- Wedding savings: $24,000 in 2 years via $500/month each.

- Travel goal: $4,000 in 8 months by saving $500/month.

- Debt payoff: $10,000 in 2 years with ~$417/month.

Investment Considerations for Long-Term Success

For long-term goals, investing can offer higher returns than savings accounts. Options like the stock market or real estate are common choices.

These assets come with risks, such as potential value loss, but can grow wealth over time. Higher rate of return than savings makes them suitable for decades-long horizons.

Tax-advantaged accounts like 401(k)s or IRAs enhance growth through compound interest. Always assess risk tolerance and diversify to mitigate downsides.

Consulting a financial advisor can help tailor investments to your specific goals. Remember that liquidity is lower, so funds should be committed for the long haul.

Psychological Techniques to Stay Motivated

Maintaining motivation over years requires mental strategies beyond numbers. Writing a letter to your future self can visualize success vividly.

Imagine how achieving each goal will feel and explore consequences of failure. Create if/then plans for obstacles to prepare for challenges ahead.

Regular communication with family keeps everyone aligned and supportive. Celebrating milestones, no matter how small, reinforces positive behavior.

These techniques turn financial planning from a chore into an inspiring journey. They help sustain effort through ups and downs in life.

Conclusion

Setting short, medium, and long-term financial goals is a powerful step toward autonomy. It transforms vague aspirations into a clear, actionable path forward.

By using frameworks like SMART and prioritization, you can navigate complexities with confidence. Automate and track your progress to ensure consistency and adaptability.

Remember, financial planning is not just about money; it's about building the life you envision. Start today, take small steps, and watch your goals unfold into reality over time.